SBCRE loans provide alternative, flexible solutions for borrowers who don’t fit traditional bank underwriting using real income, custom terms, and practical qualification methods.

SBCRE Video Overview

What is SBCRE Financing?

- Commercial real estate loans for small businesses and investors

- Used for purchase, refinance, or property improvements

- Designed for borrowers who may not meet traditional bank standards

- Offers:

- Flexible qualification criteria

- Alternative income verification (bank statements, P&L, etc.)

- Customized loan structures

Eligible Properties Can Include

Mixed Used

Retail Spaces

Office Building

Warehouse

Light Industrial

Automotive Properties

Restaurants & Bars

Daycare Centers

Mobile Home Park

Hospitality (case by case)

And Much More.... Contact Us and See if your Property Will Qualify!!!

How are SBCRE Underwritten?

SBCRE are underwritten in a similar fashion as a DSCR loan (to learn about DSCR loans click here). However, the calculation of the DSCR ratio and the necessary documentation will change based on the deal.

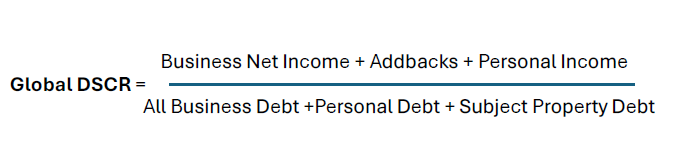

The principal ratio for SBCRE properties is based on the Global Debt Service Coverage Ratio (Global DSCR). This ratio equates to all Incomes, divided by the cost of servicing all debt. Both business and persons. It is usually applied for Owner Occupied Investments.

1. Global DSCR Formula (Owner Occupied Investment)

Formula

All Income Definition

Income generated by the business in the property, Add Backs, Personal Income

- Business Income after expenses

- Add Backs (depreciation, interest, amortization)

- Owner Salary

- Other Personal Income (W2, Passive, etc)

Total Debt Service Definition

All debt service owed by the business, personally and the property itself

- Business Loans

- Personal Debt (credit card, auto, mortgages)

- Any contingent liabilities

- The real estate loan payment

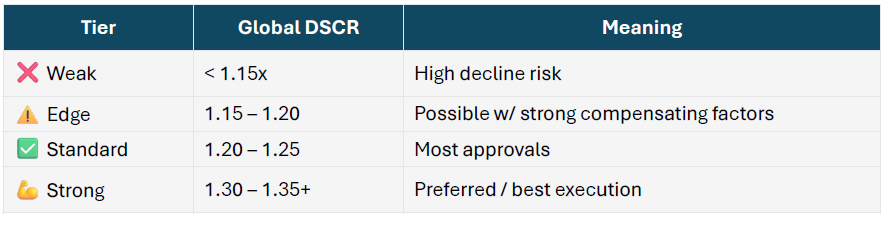

Sample Global DSCR Decision Matrix

A typical SBCRE will require a credit score of 660+

2. Simple DSCR Formula (Non-Owner Occupied)

Depending on the lender they may use the simple DSCR formula to underwrite the deal. Please explore our DSCR page for more information on how the Simple DSCR formula works.

Sample Documentation Requirements

Regardless of whether the deal is owner-occupied or not, due to the commercial nature of the financing, be prepared for this type of documentation.

Owner Occupied - Full Doc

- 3 years business & personal tax returns

- Current P&L

- Balance sheet

- Debt statements

- Appraisal

Owner Occupied - Lite Doc

- 12 months business bank statements

- Debt statements

- Appraisal

Non-Owner Occupied - Full Doc

- 3 years tax returns

- P&L and balance sheet

Non-Owner Occupied Lite - Doc

- Lease agreements only

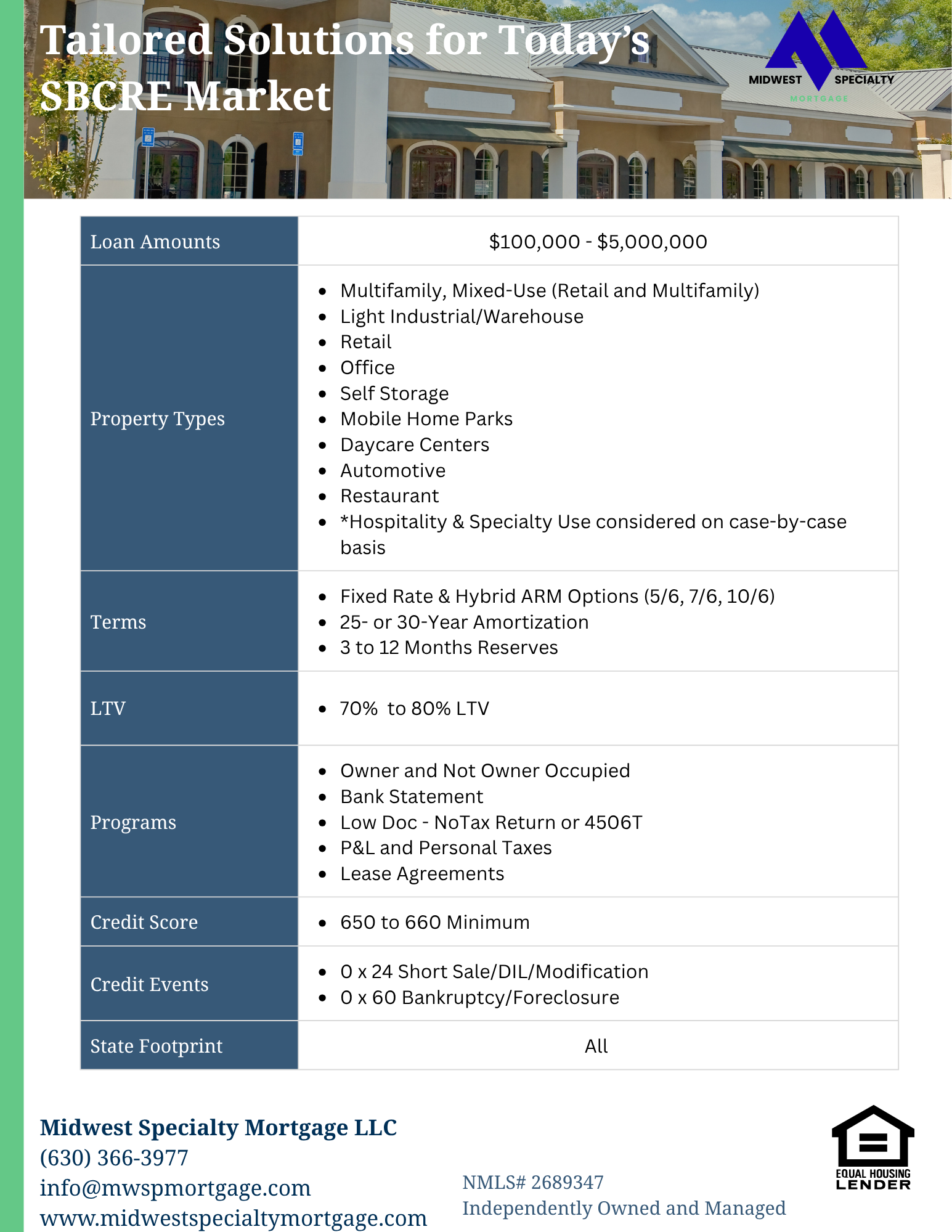

Typical Terms Available

- Fixed Rate

- Hybrids

- ARM Options (5/6, 7/6, 10/6)

- 25 to 30 year Amortization

- 3 to 12 month reserves (based on deal)

Why Choose Non-Bank SBCRE Financing?

Value Propositions:

- Faster closings (as quick as 2–4 weeks)

- Focus on deal + real income, not just tax returns

- Flexible underwriting (property-level focus)

- Most Lenders Accept:

- Self-employed / 1099 borrowers

- Mixed-use properties

- Non-standard tenants

- Can approve:

- Lower DSCR deals (1.0–1.10 range in some cases)

- Ideal if:

- Bank declined the deal

- Income is underreported on taxes

SBCRE Pre-Qualification Request

Frequently Asked Questions

What is an SBCRE loan?

An SBCRE (Small Business Commercial Real Estate) loan is a financing solution for purchasing, refinancing, or improving income-producing commercial properties used by businesses or investors.

Who qualifies for an SBCRE loan?

SBCRE loans are ideal for:

- Business owners purchasing or refinancing a property

- Real estate investors

- Self-employed borrowers and 1099 earners

- Borrowers who don’t meet traditional bank guidelines

Who qualifies for an SBCRE loan?

SBCRE loans are ideal for:

- Business owners purchasing or refinancing a property

- Real estate investors

- Self-employed borrowers and 1099 earners

- Borrowers who don’t meet traditional bank guidelines

What credit score do I need?

- Most SBCRE loans start around 660–680 FICO

- Better pricing and leverage at 700+

- Some deals may work lower with strong cash flow and equity

How much do I need for a down payment?

- Typical: 20%–30% down

- Strong deals: as low as ~20%

- Higher-risk deals: 25%–35%+

Down payment depends on:

- Property cash flow (DSCR)

- Credit profile

- Experience

- Property type

What types of properties are allowed?

Common eligible properties include:

- Retail spaces

- Office buildings

- Mixed-use properties

- Warehouses / industrial

- Restaurants and automotive

- Self-storage and specialty-use properties

Can I qualify if I’m self-employed?

Yes — SBCRE loans are designed for:

- Self-employed borrowers

- Business owners

- 1099 income earners

You can qualify using:

- Bank statements

- Profit & Loss statements

- Business financials

How is income calculated?

It depends on occupancy:

- Owner-occupied: Global DSCR (business + personal income vs total debt)

- Non-owner-occupied: Property cash flow (simple DSCR)

What is DSCR and why does it matter?

DSCR (Debt Service Coverage Ratio) measures whether income covers debt:

DSCR = Income ÷ Debt Payments

- 1.20+ → strong approval

- 1.00–1.20 → possible with compensating factors

- Below 1.00 → more challenging

How long does it take to close?

- Typical timeline: 2–4 weeks with non-bank lenders

- Banks may take significantly longer

Why not just go to a bank?

Banks:

- Lower rates, but strict guidelines

- Require perfect tax returns and financials

SBCRE lenders:

- Flexible underwriting

- Focus on the deal, not just paperwork

- Faster closings

- Work with real-world income

What documentation is required?

Depends on the loan type:

Common items:

- Business and/or personal tax returns

- P&L and balance sheet

- Bank statements

- Lease agreements (if applicable)

- Appraisal

Lite doc options may be available depending on the deal.

Can I use this for mixed-use properties?

Yes. SBCRE loans are one of the best solutions for mixed-use deals that banks often decline.

Can I refinance with an SBCRE loan?

Yes. Options include:

- Rate & term refinance

- Cash-out refinance

- Equity extraction for expansion

How much can I borrow?

- Typically $100K to $5M+ (depending on the lender)

- Amounts limitations are based on deal strength and lender credit box

- Our role is to find a lender that can meet your needs

Do I need experience in real estate or business ownership?

Not always, but:

- Experience helps

- First-time buyers may need stronger compensating factors

What are the biggest factors for approval?

- Property or business cash flow

- Down payment / equity

- Credit profile

- Experience

- Liquidity / reserves