Affordable Manufactured Home Loans in Illinois

Get approved fast with flexible loan programs designed for mobile and manufactured home even with non-traditional income.

Overview Video

A manufactured home is a factory‑built home constructed after June 15, 1976, in compliance with HUD (U.S. Department of Housing and Urban Development) standards. These homes are built in controlled environments and transported to their final location.

Manufactured homes are different from:

- Mobile homes (pre‑1976 construction)

- Modular homes (treated like site‑built homes for financing)

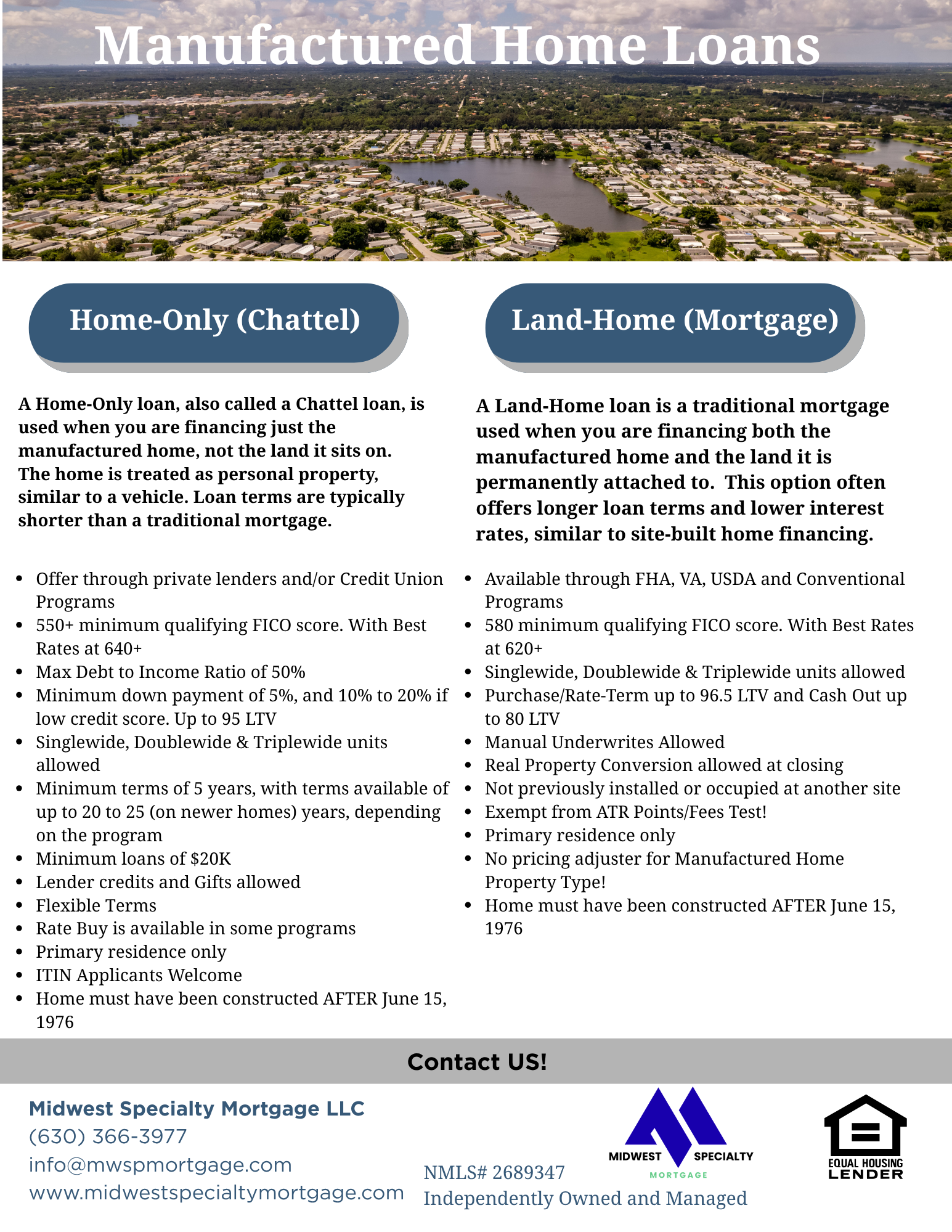

Because of how they are titled and installed, manufactured homes can be financed in two distinct ways, each with its own rules.

The way a manufactured home is titled and whether land is owned determines which financing option applies.

(Personal Property Financing)

What Is a Chattel Loan?

A chattel loan finances the manufactured home only, not the land. The home is treated as personal property, similar to a vehicle.

Common Uses:

- Homes located in manufactured home parks

- Borrowers leasing the land

- Homes not permanently affixed to land

Characteristics:

- Shorter loan terms

- Higher interest rates than mortgages

- Faster approvals

- Fewer documentation requirements

Limitations:

- ❌ No land ownership included

- ❌ Limited refinance and equity options

- ❌ Higher monthly payments

- ❌ Appreciation potential depends on market conditions

Chattel loans are popular for affordability and speed but are generally best for buyers who do not plan to own land.

(Manufactured Home Mortgages)

What Is a Real Property Loan?

A real property loan finances the manufactured home and the land together, treating the home like traditional real estate.

Requirements Typically Include:

- Home permanently affixed to a HUD‑approved foundation

- Borrower owns the land

- Home titled as real property

- HUD compliance documentation

Advantages:

- Lower interest rates

- Longer loan terms (up to 30 years)

- Equity growth and refinance options

- Better long‑term affordability

Limitations:

- ❌ More documentation required

- ❌ Longer approval process

- ❌ Property must meet foundation and zoning requirements

This option is ideal for buyers planning long‑term homeownership and future refinancing.

Manufactured home loans—especially Non‑QM programs—are flexible but still require careful structuring.

Common Lending Considerations:

- Home must meet HUD standards

- Age and condition of home may apply

- Title classification matters (personal vs real property)

- Credit score and down payment requirements vary

- Location and land ownership affect eligibility

Working with a lender experienced in manufactured housing and Non‑QM guidelines can help avoid unnecessary delays or denials.

Ask yourself:

- Do I own the land, or will I lease it?

- Is the home permanently installed?

- Do I need flexible income documentation?

- Will I want to refinance or build equity later?

The right loan depends on both the property—and your financial profile.

Chattel Only Pre-Qualification Form

Frequently Asked Questions

What is a manufactured home loan?

What is a chattel loan for a manufactured home?

A chattel loan is a type of financing where the manufactured home is considered personal property, similar to a vehicle. The loan covers only the home itself and not the land it sits on.

What is a chattel loan?

What are the main differences between chattel and real property loans?

The main differences are:

- Ownership classification (personal property vs real estate)

- Interest rates

- Loan terms

- Down payment requirements

- Consumer protections

- Refinancing and resale value

How is a chattel loan different from a traditional manufactured home loan?

The main difference comes down to ownership and classification:

- Traditional Loan (Real Property):

- Covers both land and home

- Typically offers lower interest rates

- Longer repayment terms (up to 30 years)

- Chattel Loan:

- Covers the home only

- Usually has higher rates

- Shorter terms (15–25 years)

Are interest rates higher on chattel loans?

Yes. Chattel loans typically have higher interest rates because they are considered higher risk by lenders. Real property loans usually offer lower, mortgage‑style interest rates.

Can I get financing for a manufactured home?

Yes, there are several financing options available, including:

- Conventional loans

- FHA loans

- VA loans (for eligible veterans)

- USDA loans (in approved rural areas)

- Chattel loans for home-only financing

Your approval depends on your credit, income, and property setup.

Which loan option has longer repayment terms?

- Chattel loans: Typically 15–25 years

- Real property loans: Can be 30 years, similar to conventional mortgages

Longer terms often result in lower monthly payments.

Which loan option has longer repayment terms?

- Chattel loans: Typically 15–25 years

- Real property loans: Can be 30 years, similar to conventional mortgages

Longer terms often result in lower monthly payments.

Do I need to own the land?

No. You can finance a manufactured home in two ways:

- Land ownership: Enables traditional mortgage options

- Leased land: Typically requires a chattel loan

Owning land usually results in better loan terms and long-term value.

What credit score is required?

General guidelines include:

- FHA: 580 or higher

- Conventional: 620+

- VA/USDA: around 600+

- Chattel loans: may allow scores as low as 550

Stronger credit helps you secure better rates and lower costs.

Down payment amounts vary by program?

- FHA: 3.5%

- Conventional: 3–5% or more

- VA: 0% down for qualified buyers

- USDA: 0% down in eligible areas

- Chattel loans: typically 5–20%

Can I buy land with a chattel loan?

No. A chattel loan does not finance land. If you want to purchase both the land and the manufactured home together, a real property loan is required.

What qualifies as a manufactured home?

To qualify for financing, the home must:

- Be built after June 15, 1976

- Meet HUD construction standards

- Have a HUD certification label

Older homes may not qualify for standard loan programs.

When is a chattel loan necessary?

A chattel loan is typically required if:

- The home sits on leased land

- It is not permanently attached to a foundation

- It is classified as personal property instead of real estate

Does the manufactured home need to be on a permanent foundation?

- Chattel loan: Not required

- Real property loan: Yes, the home must be permanently affixed to a foundation and meet local and lender requirements

Can I refinance my loan?

Yes. Refinancing can help you:

- Lower your rate

- Reduce your monthly payment

- Access home equity (if eligible)

You may also be able to transition from a chattel loan to a traditional mortgage if you buy land and convert the home to real property.

Can I qualify with lower credit?

Yes, there are options for borrowers with less-than-perfect credit, including:

- FHA programs with flexible guidelines

- Chattel financing with lower minimum scores

- Higher down payments to offset risk

Is mortgage insurance required?

This depends on the loan type:

- FHA loans include mortgage insurance (MIP)

- Conventional loans require PMI with less than 20% down

- VA loans don’t require monthly mortgage insurance

- USDA loans include a guarantee fee

- Chattel loans usually don’t require PMI but may have higher rates

Is it easier to qualify for a chattel loan?

Yes. Chattel loans generally have more flexible credit requirements and faster approvals, making them appealing for buyers with:

- Lower credit scores

- Non‑traditional income

- Homes in manufactured home communities

How long does the process take?

- Traditional loans: about 30–45 days

- Chattel loans: often faster, around 2–4 weeks

Do real property loans build more equity?

Yes. Manufactured homes financed as real property tend to hold value better and build equity more like traditional homes, especially when you own the land.

How do I know which loan is right for me?

The right choice depends on:

- Whether you own (or plan to buy) land

- Budget and credit profile

- Long‑term financial goals

- Location of the manufactured home

A qualified manufactured home loan specialist can review your options.

Can I finance a used manufactured home?

Yes, as long as the home meets lender guidelines for:

- Age

- Condition

- HUD compliance

Chattel loans may offer more flexibility for older homes.

Are there property restrictions?

Yes, lenders may require:

- HUD-compliant construction

- Acceptable location (community or private land)

- Age and condition standards

Can I pay off the loan early?